Options Trading for Cash Flow

Today we’re going to walk through our approach to options trading for cash flow.

Last week we sold to open a put on NKE at the $44 strike price on the 5/8 expiration date. That weekly options trade gave us $0.54 in option premium. NKE closed trading at $44.14, so our cash secured put option expired out of the money worthless. Here’s a link to that trade. We keep that option premium and now we have that capital available again.

NKE goes ex-dividend on 6/1, so we want to be sure our next option contract expires before that. We’re going to be aggressive with our strike price again in the hopes that we’ll get assigned shares. If we get shares prior to the ex-dividend date then we’ll collect the dividend. The idea with this options trading plan is to use the option premium to create consistent weekly cash flow. We’re going to sell a put option with a strike price that is close to the current trading price. If the price movement of NKE moves up, we’ll collect and keep the option premium. If the price movement of NKE drops below our strike price, we’ll still keep the option premium, but we’ll also be in a position to purchase the shares at our strike price. That will also give us the opportunity to collect the dividend.

We’re only making this trade because we’re happy to purchase shares of NKE at the strike price we select. If we are not happy to buy shares of a company at the strike price, we will not sell to open the put option contract. We generally want to use this investing approach when we have a company that we want to own for the long term that is trading at a price we’re comfortable buying shares. We’re also using only one tranche of the capital we’re willing to allocate to the company. For us, one tranche represents about 15-20% of the capital we have available to buy shares of one company or index. We prefer to enter a position in pieces rather than all at once. That way we’ll be in a position to acquire more shares at a lower price if the price movement drops through our strike price.

This options trading for cash flow strategy requires us to have the risk tolerance of either buying shares of the company at our strike price or not buying shares. We’ll collect and keep the option premium for selling to open the put option contract. But we may not get the shares if the trading price stays above our strike. If we want to be assured of getting shares we can buy shares outright.

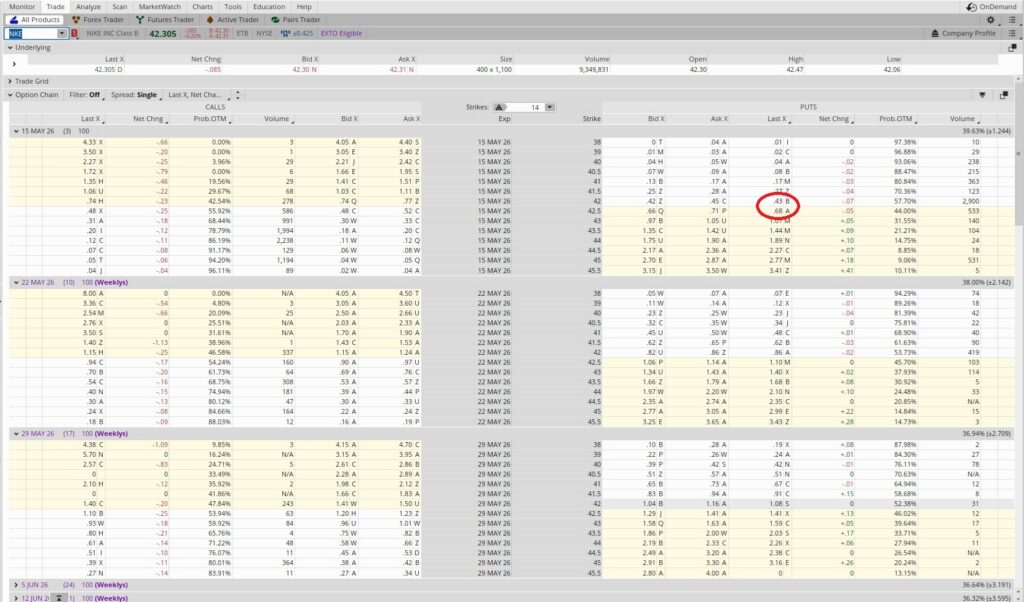

We could also sell to open a put option with a strike price that is above the current trading price. An ‘In The Money’ option contract is a contract that would be assigned at expiration if the trading price of the underlying stays where it is. If we sell to open an ‘In The Money’ option we would collect intrinsic value of the option in addition to the time decay value if we did that. Let’s walk through an example using the option chain below.

We can see the put option listed on the right side. We can see a faint yellow highlight on the lower half of each section on the right side. The strike prices highlighted in yellow are currently in the money. With NKE trading at $42.30, the put option at the $42.50 strike is in the money, while the put at the $42 strike is out of the money. The mark for the $42.50 put on the 5/15 expiration date is $0.68. With NKE trading at $42.30, the trading price is $0.20 in the money. So while the premium is $0.68, $0.20 of that is for the intrinsic value of the contract. That means we have $0.48 of premium for time decay. If the trading price of NKE stays below the $42.50 strike price our effective purchase price will be $42.50 – $0.68 premium is $41.82 per share.

Now let’s look at the $42 strike. That’s still very close to the money, but this contract will have only time decay premium because the strike price is currently below the strike price. We can see the mark for the $42 strike is $0.43. So in the event of assignment that would make our effective purchase price $41.57. The put option that is in the money is giving $0.48 in premium. The put option just outside the money is giving $0.43 in premium. While the options prices differ by $0.25 ($0.68 vs $0.43), the difference in time decay premium is only $0.05.

Now let’s look at the annualized return on the option contract. When we sell to open a put option contract we’re making a promise to buy shares of the company (or index) at the strike price. We’ll have an obligation to buy shares at the strike price. While we need to be comfortable buying shares at that price, we’re also locking up our capital for the duration of the contract. We want to be sure we’re generating an acceptable return on our capital, and more than just the basic interest rate. We look at two factors when we do that.

The first factor is the duration of the contract. Today is 5/12, and we’re looking at the 5/15 expiration date, which is the third Friday of the month. This trade lasts for less than a week, but for our purposes we’ll use one week as our time period. There are 52 weeks in one year, so our time multiplier is 52.

Now let’s look at the option premium compared to the strike price. The $42 put option has a mark of $0.43. So we divide that $0.43 in option premium by the $42 strike price and we get 0.01. Then we multiply that by our time multiplier of 52 and we get 0.53. That’s an annualized return of 53% on the capital we’re risking on this trade. Here’s a link to the option contract return calculator we use. By making this trade we’re making a promise to buy shares of NKE at $42 each. We feel that NKE is worth at least that much. So we’re happy to do this weekly options trade for cash flow.

Remember that last week we sold to open the $44 put option for $0.54 in premium as part of this options trading for cash flow strategy. That weekly option trade for passive income expired out of the money on Friday. Now we’ll add the $0.43 in option premium from this weekly options trade, and we’re at $0.97 per share in passive income. If the trading price of NKE drops through our $42 strike price and we’re assigned, our actual purchase price will the $42 strike minus the $0.97 we’ve collected in option premium, or $41.03 per share. Then we’ll also be in a position to collect the dividend of $0.41 per share on 6/1. That will bring our basis down to $40.62 per share.

If we are assigned shares at the $42 strike this Friday, we’ll wait until the NKE goes ex-dividend, then we’ll sell to open a call option contract on part of our position. We’ll use the premium from that covered call to reduce our basis on the shares we own. We’ll also continue to sell to open put options just below the trading price. That way we’ll have a trade active on both sides of the trading price. This cash flow options trade will help us to reduce our basis more quickly. Here’s another post we wrote that goes into this trading strategy in more detail.